Transfer tax on shares can significantly impact your investments, especially when transferring equity or mutual fund units within a family. Understanding the nuances of this transfer tax is essential, as it determines whether you owe capital gains tax on these transactions. Under the Income Tax Act, capital gains tax on shares doesn’t apply if you gift these assets to immediate relatives, making it a tax-free family transfer when executed correctly. However, if you engage in any form of consideration, the transaction is treated as a standard transfer, triggering tax implications. Familiarizing yourself with mutual funds tax rules and relevant documentation can help ensure seamless and compliant transactions.

In financial terms, the concept of a “transfer tax on shares” often refers to fees or taxes applied when moving equity assets. This can also include intricate rules related to capital assets, like stocks and mutual funds, which may fall under distinct tax regulations such as capital gains and inheritance tax. For family transfers, nuances such as gift tax for family transactions can create opportunities for tax-free exchanges, as long as the right documentation is in place. Understanding these terms and their implications under the Income Tax Act capital gains provisions is crucial for savvy investors. Employing this knowledge can foster better financial planning and compliance when handling financial instruments.

Understanding Transfer Tax on Shares Within Families

When transferring shares or mutual funds within a family, understanding the nuances of transfer tax is essential to avoid unexpected liabilities. In India, transfers made as gifts do not incur capital gains tax, allowing family members to distribute wealth without tax implications. However, this exemption applies strictly to gifts; any form of consideration in the transfer obligates the involved parties to adhere to capital gains tax laws under the Income Tax Act.

To ensure compliant family transfers, documentation plays a critical role. Investors should maintain essential paperwork, including a signed gift deed, relationships proofs, and transaction records. This documentation is crucial in establishing the intent of the transfer and helps prevent disputes with tax authorities. Notably, while transfers between family members can streamline inheritance processes, they must be approached with understanding of the potential tax consequences if not properly executed.

Key Documents Required for Tax-Free Family Transfers

Maintaining a clear and detailed set of documents is imperative for ensuring a tax-free transfer of shares or mutual funds within a family. The Income Tax Act outlines specific requirements for a gift to qualify for tax exemptions, which include having a formal written gift deed. This document should delineate the relationship between the giver and the receiver, providing legal validity to the transfer.

Additionally, supporting documents like birth certificates or family declarations impart legitimacy to the relationship. Both the transferor and recipient must maintain records that include PAN details, bank statements, and transaction trails. This meticulous approach ensures clarity and transparency, safeguarding against potential tax audits or disputes that could arise over misunderstood transactions.

It is also beneficial to have valuation evidence on hand at the time of transfer, including the Net Asset Value (NAV) for mutual funds and market prices for equity shares. Such records will be critical should there be any future inquiry from tax authorities regarding the nature and value of the gifts transferred.

Tax Treatment of Shares and MF Units After Family Transfers

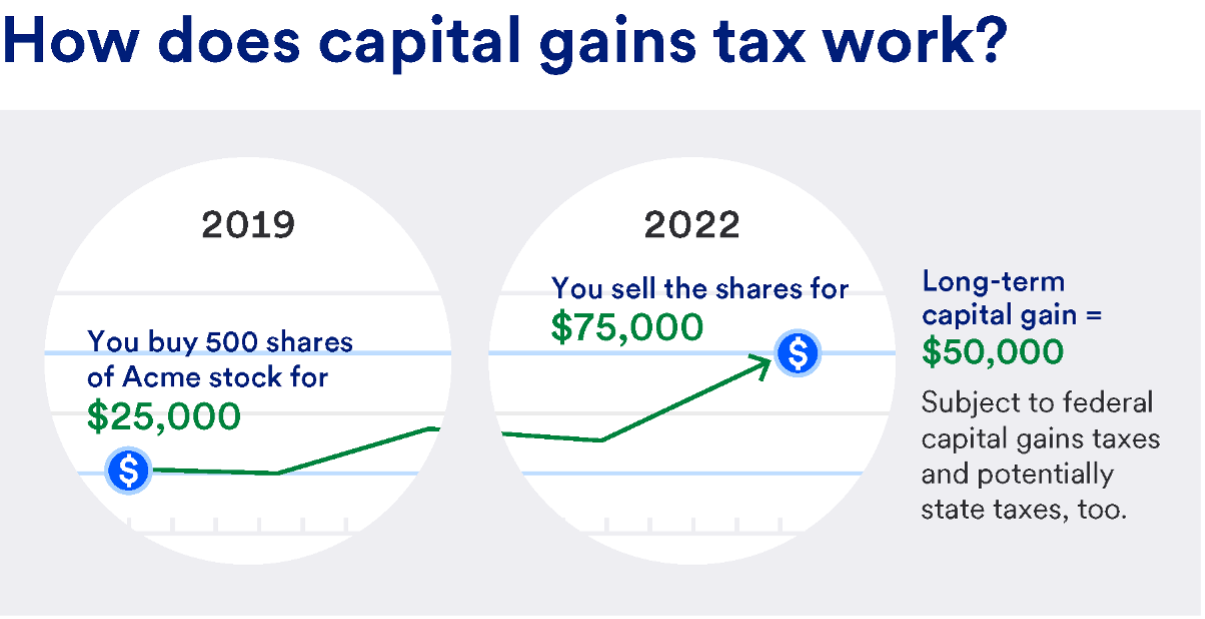

The capital gains tax implications of shares or mutual funds received as gifts carry specific rules under Indian taxation. When a family member receives shares or mutual fund units, they inherit the holding period of the original owner, which can affect the categorization of gains as either short-term or long-term. This transfer mechanism is significant because long-term capital gains (LTCG) are generally taxed at a more favorable rate compared to short-term capital gains (STCG).

Understanding the concept of holding periods can greatly influence how the recipient prepares for future transactions. If they later decide to sell the shares or units, the tax liability will be influenced not just by their ownership duration but also by the original owner’s holding period. It is crucial for families engaging in asset transfers to grasp these tax ramifications, as ultimately, proper planning can lead to significant savings and more advantageous investment strategies.

Planning for Capital Gains Tax When Selling Received Assets

When a recipient sells shares or mutual funds acquired through a family transfer, they must consider the capital gains tax provisions applicable under the Income Tax Act. The combined holding period—factoring in both the original and the current holder—can impact the overall tax liability. For example, if the original owner held the asset for over a year, the recipient may be able to enjoy long-term capital gains rates, which generally offer a lower tax burden.

Proper planning is essential for maximizing tax efficiency, particularly if the recipient anticipates selling the shares or funds shortly after receiving them. Filing tax returns using forms like ITR-2 or ITR-1, depending on the total income levels and type of gains, helps in reporting accurately while clarifying the sources of income. Engaging a tax advisor can also facilitate strategic planning around the timing of sales to minimize tax liabilities effectively.

Gift Tax Considerations in Family Transfers

Gift tax regulations play a crucial role in family transfers of shares and mutual funds. While the transfers between family members are exempt from capital gains tax, it is essential to be mindful of the nuances of gift taxation, particularly under the current laws. For instance, any gift exceeding a certain threshold might trigger a gift tax liability, depending on the valuation of the assets transferred.

It is important to assess the total value of gifts within a financial year and document them thoroughly to avoid any unexpected tax implications. Keeping all necessary records and understanding the limitations of tax-free gifts can prevent future disputes and ensure a smooth transition of assets among family members. In doing so, investors can make informed decisions that align with their financial strategies and familial commitments.

The Importance of Family Relationships in Asset Transfers

Family relationships serve a vital role in how asset transfers are treated concerning capital gains and gift taxes. The Indian Income Tax Act provides favorable conditions for immediate relatives, including exemptions on capital gains tax when assets are transferred as gifts. This favorable treatment underscores the importance of familial bonds in financial planning and wealth distribution.

Recognizing that these transfers can be executed seamlessly fosters a culture of financial support within families. However, transparency and documentation remain paramount to ensuring compliance with tax laws. By upholding a clear understanding of relationships and fraternal obligations, families can navigate the complexities of tax treatments during asset transfers, thereby promoting financial literacy and strategic inheritance.

Insights into Mutual Funds Tax Rules

Mutual fund tax rules are particularly relevant when it comes to understanding how fund units are taxed post-transfer. Similar to shares, mutual funds can be transferred without capital gains tax implications if done through gifting among family members. This aspect not only simplifies the transfer process but also encourages investments within families, allowing them to build wealth collectively.

Tax implications further diverge if the recipient later decides to sell the mutual fund units. Understanding the taxation landscape, including long-term versus short-term capital gains considerations, is crucial for any recipient planning to manage their financial portfolio wisely. By familiarizing themselves with mutual fund tax rules, families can optimize their investment strategies and thoughtfully navigate inheritance matters.

Navigating Tax-Free Family Transfers with Care

While tax-free family transfers present a unique opportunity for wealth distribution, they must be navigated with caution. Families looking to transfer shares or mutual funds without incurring capital gains tax should ensure that the transfer strictly adheres to conditions set forth under the Income Tax Act. This includes maintaining necessary documentation, such as a valid gift deed and proof of relationship, to validate their intentions.

Moreover, families should seek to understand all related tax regulations, including implications surrounding capital gains and asset valuation. Planning these transfers not only ensures adherence to tax laws but also enhances the legacy left for future generations. Open discussions and clear agreements among family members reinforce the process, leading to smoother transitions and mutually beneficial financial outcomes.

The Evolving Landscape of Transfer Taxes

The evolution of transfer taxes presents families with new challenges as well as opportunities. The recent amendments to the Income Tax Act have clarified many rules surrounding capital gains tax and family transfers, making it imperative for investors to stay informed about such changes. As financial dynamics shift, understanding these laws will enable families to make strategic decisions that maximize their financial outcomes.

As more families engage in wealth redistribution via share and mutual fund transfers, staying up-to-date on tax implications becomes increasingly critical. Taking advantage of current tax laws can help families minimize liabilities and harness opportunities for growth. Individuals are encouraged to seek professional advice to navigate these evolving laws effectively and to establish a robust financial future for all family members.

Frequently Asked Questions

What is the transfer tax on shares when gifting them to family members?

When equity shares or mutual funds are transferred to family members as gifts, they are typically exempt from capital gains tax, according to Section 47 of the Income Tax Act. However, it’s crucial to ensure that the transfer is made without consideration to qualify for this exemption.

How does capital gains tax on shares work when the recipient sells them?

If shares or mutual funds are received as a gift, the original owner’s holding period is carried over to the recipient, which helps determine the applicable capital gains tax when they sell the shares. This means if the original owner held the shares for a long-term period, the recipient can benefit from the lower long-term capital gains tax rates.

Are there any tax implications under mutual funds tax rules for family transfers?

Yes, mutual funds tax rules stipulate that transferring mutual fund units to family members without consideration is treated as a gift, thus exempting it from capital gains tax. It’s essential to maintain proper documentation to support the transaction’s nature.

What documentation is necessary to avoid tax disputes when transferring shares as gifts?

To avoid tax disputes during the transfer of shares or mutual funds as gifts, maintain a signed gift deed, proof of relationship, bank and demat statements showing the transaction, and purchase proof. These documents will substantiate the tax-free nature of the transfer.

Can I be subject to gift tax for family transfers of shares?

Generally, transfers of shares within family members as gifts are exempt from gift tax under the current laws, provided they are made without any consideration. However, it is wise to consult a tax professional for specific cases to ensure compliance with the latest regulations.

What is the treatment for capital gains tax when shares are sold after a family transfer?

When shares or mutual funds are sold after being transferred as gifts, capital gains tax is assessed based on the original owner’s holding period. This rule under the Income Tax Act helps determine whether the gains are short-term or long-term, impacting the tax rate applied.

How do tax-free family transfers of shares affect the tax liability of the recipient?

In tax-free family transfers of shares, since the transfer is classified as a gift, the recipient enjoys the benefit of the original owner’s holding period when they sell the shares, potentially resulting in lower tax liability if the shares qualify for long-term capital gains.

| Key Point | Details |

|---|---|

| Transfer Tax Exemption | Transfers between family members as gifts are tax-free under Section 47 of the Income Tax Act. |

| Consideration in Transfer | Transfers with consideration (e.g., selling shares) are taxable as capital gains. |

| Documents Required | Maintain a written gift deed, proof of relationship, PAN details, transaction statements, and valuation proof. |

| Holding Period for Taxation | The recipient’s holding period is based on the original owner’s duration for capital gains tax purposes. |

| Filing Tax Returns | ITR-2 is for capital gains; ITR-1 can be used if income is under ₹50 lakh, with limitations on gains reported. |

Summary

Transfer tax on shares is a critical aspect for investors considering asset transfers within families. When equity shares or mutual funds are gifted, they can be transferred without incurring capital gains tax, provided specific documentation and relationship proof are maintained. Understanding these regulations helps in legally maximizing tax benefits while minimizing disputes on share transfers.